The “Term sheet” carries an air of mystery and intrigue in the entrepreneurial community. Founders are either nervous or giddy about them, want to get one and celebrate its arrival. Investors are eager to sign them (while tending to wait for a lead investor to generate them).

Working with startups and angels in my community gives me a perspective on term sheets. Since the landscape that governs capital here is markedly different than that in VC hotspots, I’m sharing the elements I see ignored/problematic/contentious, here, in Des Moines, Iowa.

Disclaimer: Getting introduced to Brad Feld’s Venture Deals, following a number of blogs, and ultimately digging through dozens (hundreds now?) of term sheets, I feel like the 4-10 page document is boiled down to a few critical elements that trip up entrepreneurs and angel investors alike. I am not a VC, nor do I represent a fund, so the motivators behind VC decisions are still largely remote to me.

Oh, and also – I am not a securities attorney – use this as a starting point in your journey on term sheet education but seek competent advice at the time you begin working with these documents.

What is a term sheet?

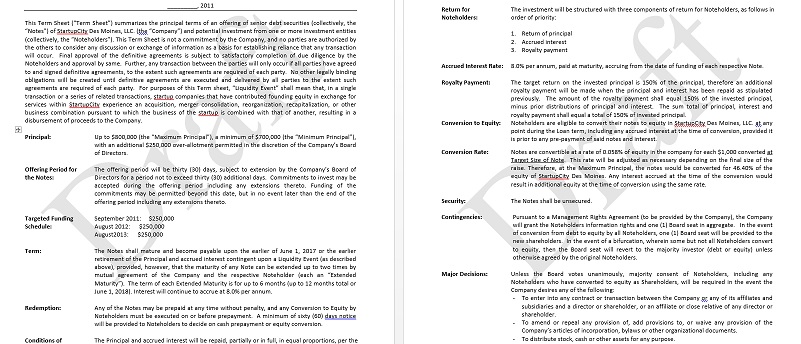

When an entrepreneur chooses to accelerate the journey of building or scaling a business with outside capital, the term sheet is a formal document that outlines the summary terms of exchanging a portion of the company (equity) for cash from an investor (investment). Though filled with legalese about a variety of important topics, it sets the initial terms of engagement, specifically through core elements that would fit on a napkin.

The elements boil down to three simple drivers – economic, team and control. Drivers that control the money aspects of the transaction, those detailing the people building the company, and how the power will be shared once the investment is initiated, respectively.

Economics (equity, valuation…)

Though it should come later, this is frequently the starting point of a negotiation. A placeholder for the amount the two parties think a company is worth, valuation is a key point of the negotiation. Of course, like any parent, the entrepreneur values their company higher than the dispassionate observer. Similarly, the investor tries to justify the entrepreneur’s assessment or comes up with their own yardstick for evaluation. The mid-western investor rarely puts down a $1M or higher value on a company that has no product, no real customers, and an incomplete team. Ideas alone seem to rarely receive outside funding, and when they do, the term sheets are skewed toward a great deal of control in the investor’s hands for significant share of equity.

What’s an entrepreneur to do? If the desire is to raise local money and not travel nationwide pitching to investors, then appealing to the local investors motivators is key. Those motivators, at this point in time, are product, revenue, and team:

- Product – a company needs a minimum viable product (MVP) that demonstrates the founding team’s vision. It must be usable, demonstrable, available on the relevant platform (web, mobile, physical goods etc.), and one or more customers be able to speak to its viability and use.

- Customers – Revenue comes from customers, so this is important. The history of a product’s sale to an unrelated customer — one with whom the entrepreneur didn’t have an established relationship –is important. Customers provide external validation of an idea and are key to an investor’s ability to preview a product’s market viability.

- Team – a complete team is generally a pre-requisite for a company raising funds and must include founder (with a concrete role – not just title) marketing, product development, and ability to execute. These people and roles will change over time, so, a complete team needs to reveal the people who fill to roles to adequately guide the minimum viable company to the market where their products are sold, licensed, and used by real customers.

- Exit – there will be discussion, however premature it may seem, about the liquidity or liquidation event. It could be brief, or a full buy-sell analysis, but there will be one. READ THIS CAREFULLY, especially the section related to liquidation preference that establishes rights to the funds received at a liquidity/sale event.

Team

Though the term sheet will have a signor on behalf of the company, the team does not need titles like CEO, CTO, COO, etc. At this stage, there really isn’t a true CEO or CTO – but rather founders, builders, designers and hackers. The first developer on a team will very likely NOT be the CTO of the fully baked company — the skill sets for the two are vastly different. Similarly, the founder will very likely be replaced as the CEO over the venture-backed lifetime of the company. The team, therefore, needs to be able to present a diversity of opinion that will lead the company to grow, but show a unified front through consensus building.

Rented CEOs and other titles are a let down – angel investors invest in passionate founders, and founders who have given up critical equity for a part-time CEO in early stages of building a product can actually hurt themselves. So, for the purposes of showing off the MVP and raising capital, founders (not a bunch of rented suited professional CEOs) should demonstrate their wares . Business attorneys do a far better job negotiating terms.

Control

Once money and equity exchange hands, those providing the money will often desire control over the operation of the company in material areas. These terms change the daily behavior of the company and its founders, and must be negotiated early and clearly. If legalese in the documents is not understood, clarify – it’s a lot easier to do before the deal is done than after. Any attorney worth their salt understands that the legalese in the documents is a necessary evil, and can summarize the entire document in a page of plain English. That page is worth its weight in gold for us mere mortals. Key elements of control include such things as

- Information rights – this gives the investor a right to receive regular (quarterly or otherwise) updates from the company that summarizes financials without divulging too much information that may be proprietary. Though angel investors have significant insight into a company and operate like many insiders, this right is still necessary to document and usually a requirement for an angel investment.

- Founders salaries – investors know that the first influx of cash can alter the incentives and behavior in a company, including such major items as founder compensation as well as minor items like benefits. Thus, term sheets may dictate how much or if the founder can give themselves a raise.

- New stock/dilution – investors understand there will be dilution during successive raises but want to have a say in when/how much/rules surrounding such raises. Expect a clause allowing the angel investor to participate in future rounds to maintain their ownership percentage, participate in sale of stock by the founder, and advance warning about upcoming events that can cause dilution.

- Board Seat – though many investors would love to be on the board for their new portfolio company, angel investors in particular, frequently decide against it and choose to serve instead as informal advisers, rainmakers, network connectors, and supporters. Still, a paragraph or two will be dedicated to this element.

In closing, remember, a term sheet is not the final definitive document that guarantees an investment. It is simply the first formal document used to begin the conversation. Treat it with care.

Additional Resources

Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist

Ideal First Round Terms, Chris Dixon on cdixon.org